Why Financial Systems Are Returning to Registries

- Mar 28

- 3 min read

Across financial systems, one of the most enduring institutions is the registry. Registries record ownership, validate transactions, and provide authoritative references that financial markets depend on to function. Whether in land records, securities depositories, corporate ownership databases, or payment clearing systems, registries serve as the institutional memory of economic activity.

In recent years, however, registries have begun to attract renewed attention. As digital financial systems expand and new technologies reshape how assets are issued and transferred, policymakers and market participants are rediscovering the central role that trusted registries play in maintaining financial stability.

Historically, registries have taken many forms. Securities markets rely on central securities depositories that record ownership of equities and bonds. Land markets depend on property registries that verify title and ownership. Corporate governance frameworks use company registries to establish legal identity and accountability. In each case, the registry functions as a trusted source of truth.

The digital transformation of financial systems has not removed the need for registries. Instead, it has made them more important. As assets increasingly move onto digital platforms, the question of how ownership is verified becomes even more critical. Without a reliable mechanism for recording who owns what, financial markets cannot operate with confidence.

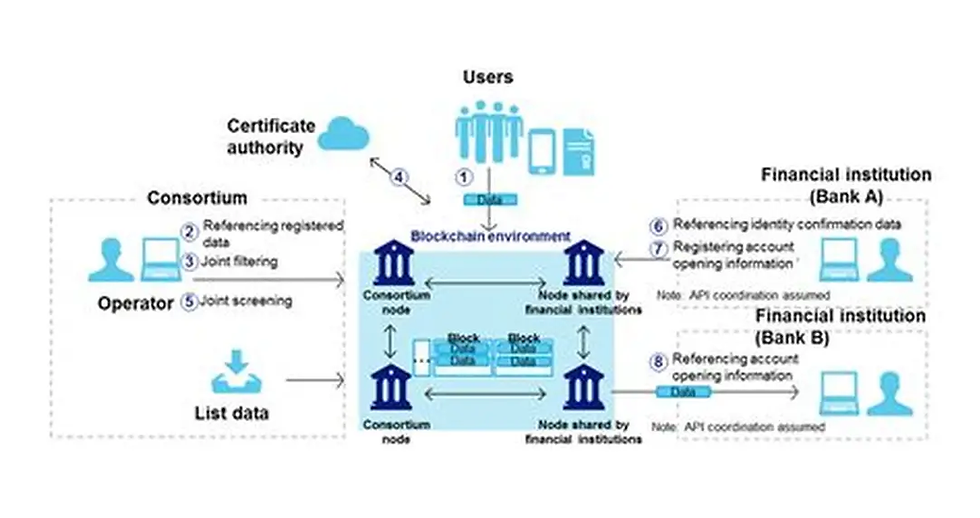

Distributed ledger technologies have often been described as alternatives to traditional registries. In practice, however, many digital asset systems are evolving into new forms of registries themselves. Rather than eliminating authoritative records, blockchain-based systems typically create shared ledgers where multiple participants maintain synchronised copies of transaction histories.

The key distinction lies not in whether registries exist, but in how they are governed. Traditional registries often rely on a single authority responsible for maintaining records. Digital registries, by contrast, may involve multiple institutions participating in a shared verification process. In both cases, trust ultimately depends on the institutional framework that oversees the registry.

This institutional dimension explains why policymakers increasingly emphasise governance rather than technology when discussing digital financial infrastructure. Registries must ensure that entries are verified, that records cannot be altered without authorisation, and that disputes can be resolved through recognised legal mechanisms.

In financial markets, registries also serve an important coordination function. When institutions rely on the same authoritative records, they can transact with confidence that ownership claims will be recognised by regulators and courts. Without such coordination, markets would face significant risks of duplication, fraud, or conflicting ownership claims.

The emergence of tokenised assets has reinforced the importance of this principle. When financial instruments such as bonds or funds are represented digitally, the registry effectively becomes the place where ownership exists. Transfers between parties must therefore update the registry in a manner that is recognised by both market participants and regulatory authorities.

Several jurisdictions are already experimenting with new forms of digital registries. Projects involving tokenised securities, digital land records, and interoperable financial databases illustrate how registry-based systems can be modernised using digital infrastructure. These initiatives often combine distributed ledger technologies with traditional governance mechanisms, creating hybrid architectures that preserve institutional oversight while improving operational efficiency.

At the international level, discussions around digital public infrastructure increasingly highlight the role of registries in enabling trust across systems. Payment networks, identity systems, and financial data exchanges all depend on reliable records that institutions can verify and rely upon. Without such records, interoperability between digital systems would be difficult to sustain.

This renewed focus on registries reflects a broader realisation about the nature of digital transformation. Technologies may change how financial transactions are processed, but the underlying requirement for trusted records remains constant. Markets require authoritative sources of information that establish ownership, validate transactions, and provide continuity over time.

In this sense, the future of digital finance may involve not the disappearance of registries but their evolution. New technologies can improve how registries operate, making them more transparent, interoperable, and resilient. Yet the core function of a registry, providing a reliable record that institutions trust, remains as essential today as it has been for centuries.

As financial systems continue to digitise, the institutions responsible for maintaining these records may become even more significant. The design of registries, their governance structures, and their interoperability across systems could ultimately determine how digital financial markets evolve in the years ahead.

References

Bank for International Settlements. The Future Monetary System and Digital Financial Infrastructure.https://www.bis.org/publ/arpdf/ar2023e3.htm

World Bank. Digital Public Infrastructure and Data Governance.https://www.worldbank.org/en/topic/digitaldevelopment

International Monetary Fund. Digital Money and Financial Stability.https://www.imf.org

Comments